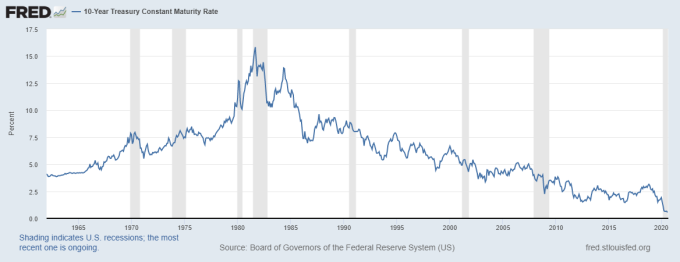

Since 2015, my forecasting models have predicted the 10-year Treasury yield would stay in the range of 1.60% to -3%. Tangential to this, the next recession treasury yields, and thus mortgage rates, would fall because lower growth would drive yields and rates lower. The four-decade prolonged downturn in the rate of growth in the economy and inflation mirrors falling bond yields and mortgage rates.

Before the pandemic, it was hard work trying to convince other economists that we would see a 30-year fixed mortgage rate below 3%. In 2018, a crafty photographer caught the bemused look on my face when one of my colleagues chastised me for predicting rates would go lower instead of higher.

Evangelizing a consistent thesis for years on end is a bit boring, but I would rather be dull and steady than the alternative. I admit I am a big fan of sticking to economic models that allow for reliable predictions, repetitive as they may be, until different variables change the course of the economy.

Today, in the middle of a world pandemic, my bond market model is allowing for a 30-year fixed mortgage rate as low as 1.875% – but the questions remain, will it, and what will it take to get there?

The post What would it take to see mortgage rates go below 2% on a 30-year fixed? appeared first on HousingWire.