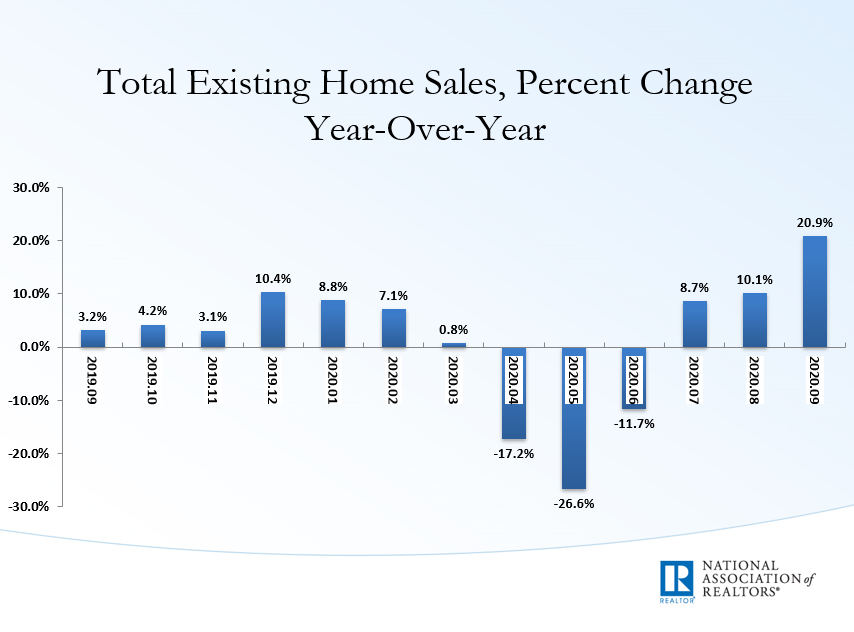

The NAR existing home sales report released today blew out all estimates with 6,540,000 in existing home sales. This epic headline punctured any 2020 bubbles the housing bubble boys had left in their arsenal. But before we get too excited, keep in mind we are still down 0.2% year to date compared to 2019 levels. Still, this seems like a booming housing market, right?

I have often claimed that 2008-2019 would have the weakest housing recovery ever in history. And it did. I also said that the new home sales recovery would be fairly anemic, housing starts would never start a year at 1.5 million and purchase applications would never hit 300 until the years 2020-2024.

Well, here we are in 2020 entering into the best housing demographic patch ever recorded in U.S. history. We have “built-in” replacement buyers at a time mortgage rates are low and are likely to remain so during the next five-year period. One might say this is a perfect storm for housing to outperform other economic sectors for years to come.Then COVID-19 happened and the chaos theory and the butterfly effect took hold of the U.S. economy back in March.

However, there are some things not even COVID-19 can take away. So, let’s take a look at the housing data in 2020 so far.

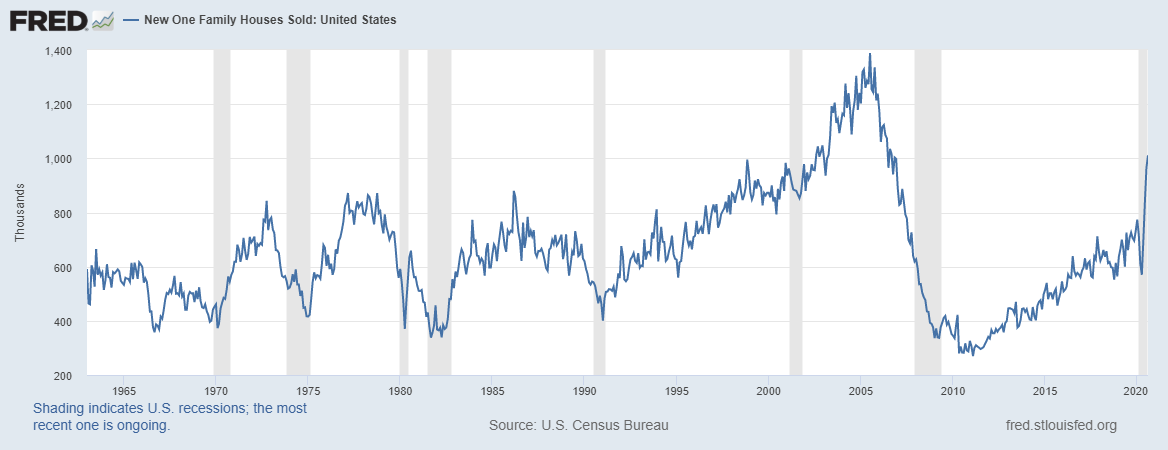

New home sales are on fire and this data line will moderate for sure. However, new home sales have outperformed my 2020 forecast as this sector benefits with lower mortgage rates than even the existing home sales market place.

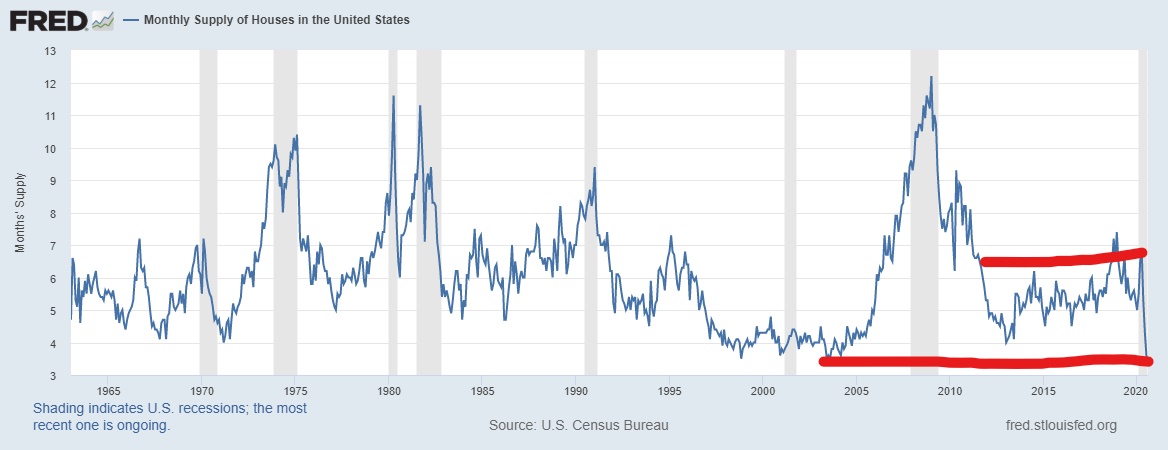

The best part about housing in 2020 for me is the monthly supply data for new home sales has moved lower. This is where monthly supply for new homes should be when new home sales demand is strong. This is good for housing starts.

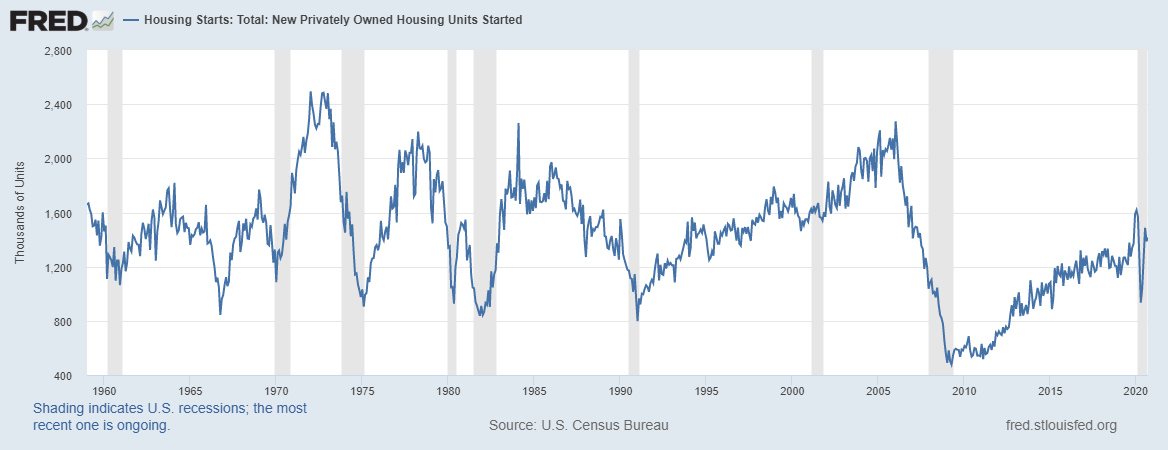

Housing starts are also up, but we haven’t started the year at 1.5 million housing starts yet. Although we have some weakness in the multifamily sector, housing starts have made an epic comeback. But we have to remember that in February it showed near 40% year-over-year growth, before COVID-19 hit. This housing story was here before COVID-19 hit us.

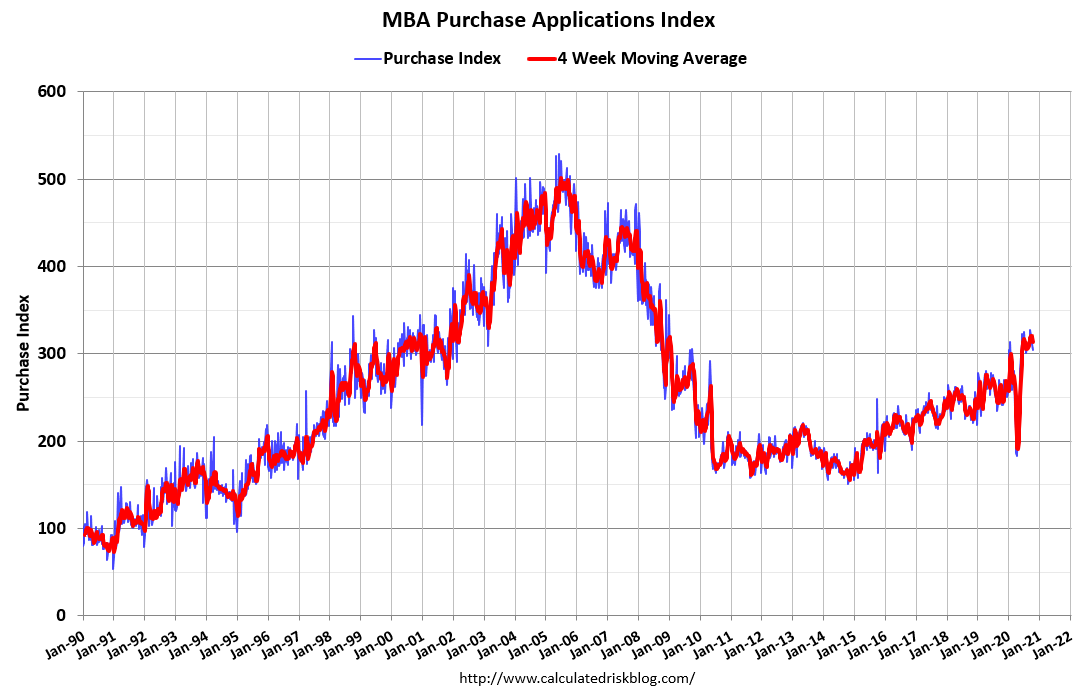

Mortgage Bankers Association purchase application data has shown us 22 straight weeks of positive year-over-year growth, averaging over 20% during the timeframe. We have finally breached the 300 level in this index in 2020 like demographic clockwork. The last four weeks of year-over-year growth were 26%, 24% ,21% and 22%. Remember, this data looks out 30-90 days.

When I think about housing 2020, it’s not the V-shaped recovery that I will remember first or the most. I will remember the February existing home sales data which got me almost spitting out my coffee. That February report was one of the most impressive I have seen in my lifetime. That was the green light that housing was going to outperform even my estimate for 2020.

In years 2020-2024, even with COVID, housing has the ability to outperform just based on the raw power of demographics. COVID-19 gave us nine weeks of negative year-over-year data followed by an undeniable housing market comeback. This happened because demographics and mortgage rates are what drive this part of the economy.

It helped too, that Freddie and Fannie weren’t publicly traded companies without government backing, so credit stress was stable as we never really had a tight lending housing market in 2020, at worst 4.5% to 6.2% of all loans were tight this year.

Today, we are back to almost flat even with the 20.9% year-over-year growth from the recent report. Yes, we went through some pretty spectacular gymnastics in housing to end up basically flat for the year.

In my opinion, if we had not been affected by the COVID crisis, existing home sales would have ended 2020 with between 5,710,000 – 5,840,000 in sales. This would have been a big jump from 2019 levels and compared to the previous years. We may not be able to make up all the lost ground due to COVID-19 this year, but that demand may be pushed forward to the next year.

For now, just know that the housing bubble boys and the mega housing bears blew it this year! Why? Because they didn’t focus on the two factors that drive the housing market: demographics and mortgage rates. Rates can go higher but demographics are very sticky and not so easy to manipulate. As you can see, this isn’t an overheating demand market compared to last year, we aren’t even positive for 2020, not yet at least.

So, don’t get too bearish if you see a housing data rate of growth slow down in the upcoming months. This has been a common failure by housing bears for many years. Remember, think of sticky demographic demand — the replacement buyers in years 2020-2024 — and if rates stay low, housing will be stable.

The post The housing bubble boys blew it in 2020 appeared first on HousingWire.