On Friday, the Bureau of Labor Statistics reported that 261,000 jobs were created and we had 29,000 positive revisions to prior reports. This means the honey badger labor market will keep the Federal Reserve from pivoting anytime soon.

This has been a theme of mine lately. Since all my six recession red flags are up, the only data lines that I am focusing on regarding the cycle of economic expansion to recession are job openings and jobless claims data. Both these data lines were solid this month, so the jobs data won’t turn damaging enough for the Fed to pivot.

The labor market is actually running into a big theme of my economic work over the years. I recently talked about it on this podcast because I wanted to remind people that early in the U.S. recovery cycle, job openings getting toward 10 million was part of my forecast. No country has a Dorian Gray labor market and the labor market deals with different dynamics as the baby boomers leave the workforce each year.

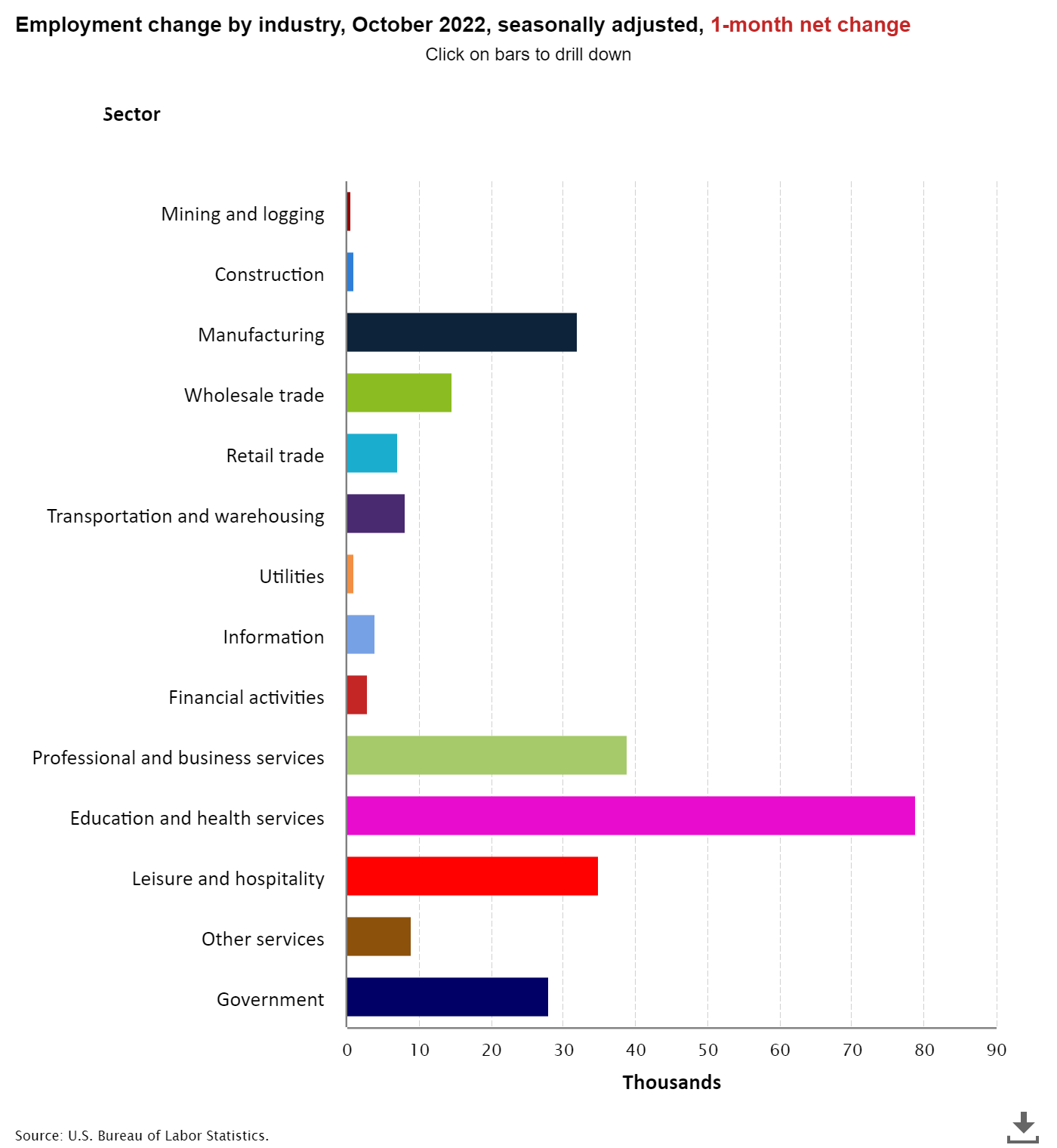

From BLS: Total nonfarm payroll employment increased by 261,000 in October, and the unemployment rate rose to 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in health care, professional and technical services, and manufacturing.

The unemployment rate did rise from 3.5% to 3.7%; this happened once before this year when we saw the unemployment rate pick up among people who had never finished high school. The following month it reverted back to 3.5%.

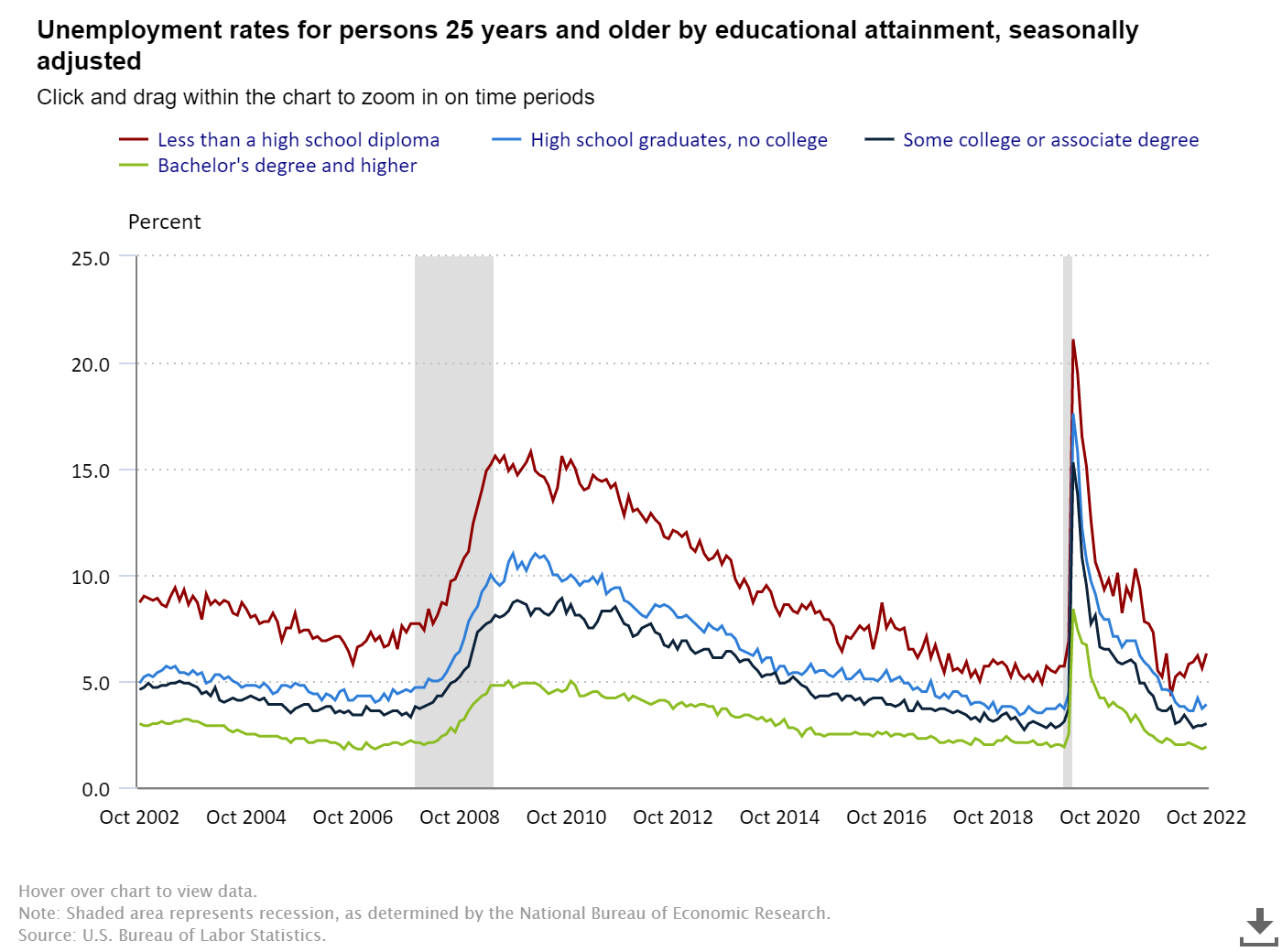

Below is a breakdown of the unemployment rate and educational attainment for those 25 years and older.

- Less than a high school diploma: 6.3%. (previous 5.6%)

- High school graduate and no college: 3.9%

- Some college or associate degree: 3.0%

- Bachelor’s degree and higher: 1.9%

The unemployment rate can rise if the labor force pool grows while still creating jobs. I advise you not to read too much into one month’s data until it becomes a trend. Of course, regarding the Fed’s pivot, jobless claims need to get to 323,000 on a four-week moving average for me to believe that the Fed will take notice of an economy going into recession.

Since I have all six recession red flags up now, I am keeping an eye on jobless claims data first because once it breaks higher, the job-loss recession has begun, something we’ve seen in every economic expansion-to-recession cycle.

Below is a breakdown of the jobs created this month. As you can see, the construction sector was barely positive; this is one area of the marketplace that should be losing jobs next year. The builders are now holding onto their labor due to the backlog of homes under construction. When that ends, they will join the ranks of others in the housing industry that are laying off people.

Remember, housing went into recession in June of this year and we haven’t had 12 months of recessionary layoffs in the system yet.

All six of my recession red flags are up, so these are data lines that people should be tracking:

Job openings

The Fed would love to see this data line go down. Before COVID-19, job openings were over 7 million, and we didn’t have to deal with inflation. The Fed believes higher unemployment means people get paid less, which is why they want to fight inflation. The most recent job openings report showed an increase to 10,717,000.

Jobless claims

This data line is essential for the general economy because the Fed can keep discussing higher rates or keeping rates high until the labor market breaks. Once jobless claims break, the discussion changes. That level is 323,000 on the 4-week moving average. We aren’t there yet, and jobless claims fell this week to 217,000.

At this point, is there any way to prevent a recession? Once all six recession red flags are up, history is not on our side. However, due to the crazy swings that this COVID-19 recovery has given us with the wild bullwhip effect on data, I have come up with some plausible theories. Here are the two ways we can avoid this recession:

1. Rates fall to get the housing sector back in line. Mortgage rates falling toward 5%, as we saw earlier in the year, can be a stabilizing factor for housing if they can have duration. Traditionally, mortgage rates below 4% boost housing demand. However, first things first: the bleeding needs to stop.

2. The inflation growth rate falls, and the Fed stops hiking rates and reverses course, as it did in 2018. Some of the inflation data is already cooling off and will find its way into the data lines. However, rent inflation won’t come down in the data until 2023, even though we already see some coolness in that sector.

Is there any hope that one of these things happen and we avert this recession? If we don’t have any more supply shocks like we experienced after the Russian invasion of Ukraine or from other variables that aren’t tied to the economy, the growth rate of inflation should be falling next year due to rent inflation falling. I talked about it on CNBC recently. If that happens, if the Fed starts to pivot and then cuts rates as they did in 2018, we might have a shot here.

Of course, it’s very late in the year now, so this is more or less a 2023 storyline, but I outline my best case for mortgage rates to fall next year in this article.

However, history has never been on our side once the six recession red flags are up. There is a first time for everything, but most people are now employed, and household balance sheets look much better now than we saw in 2005-2008. At this point it’s all about timing. However, the longer we go with higher rates, the less chance of a soft landing.