Today, the Bureau of Labor Statistics reported that 467,000 jobs were created in January. This was a big surprise as some people, including me, thought the rise in the number of sick days being reported could impact this month’s job report. One of the factors I’ve cited over the last few months is that we should see more positive revisions occur in the future. The total positive revisions in this report are 709,000.

To say that I was excited to see this report is an understatement. Since the economic lows in April of 2020, it has been a joy to see my country make the most significant economic comeback ever. What I wrote on April 7, 2020, I truly believe on the economic front: “My faith in America winning has never let me down because I always believe in my people and country. I can tell you now, this virus isn’t changing my view on that.”

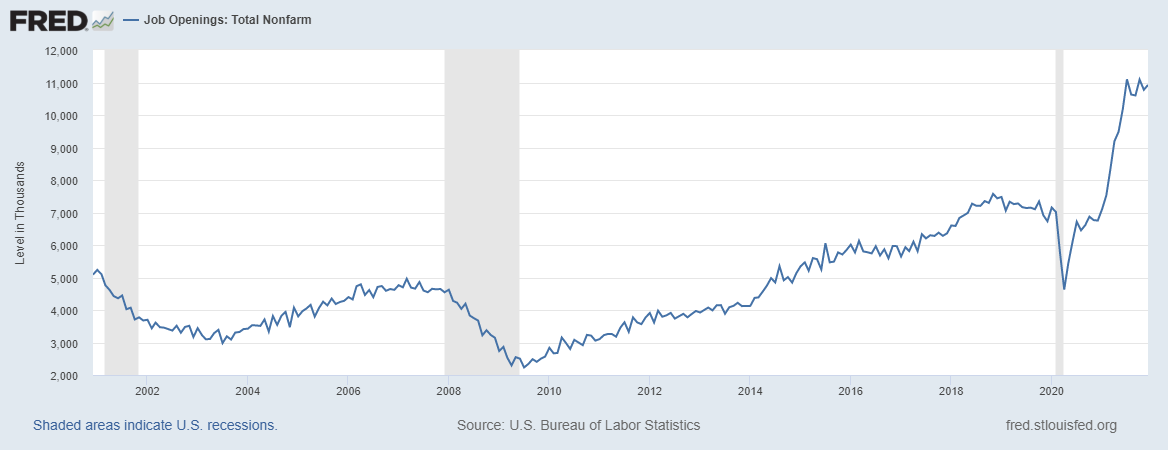

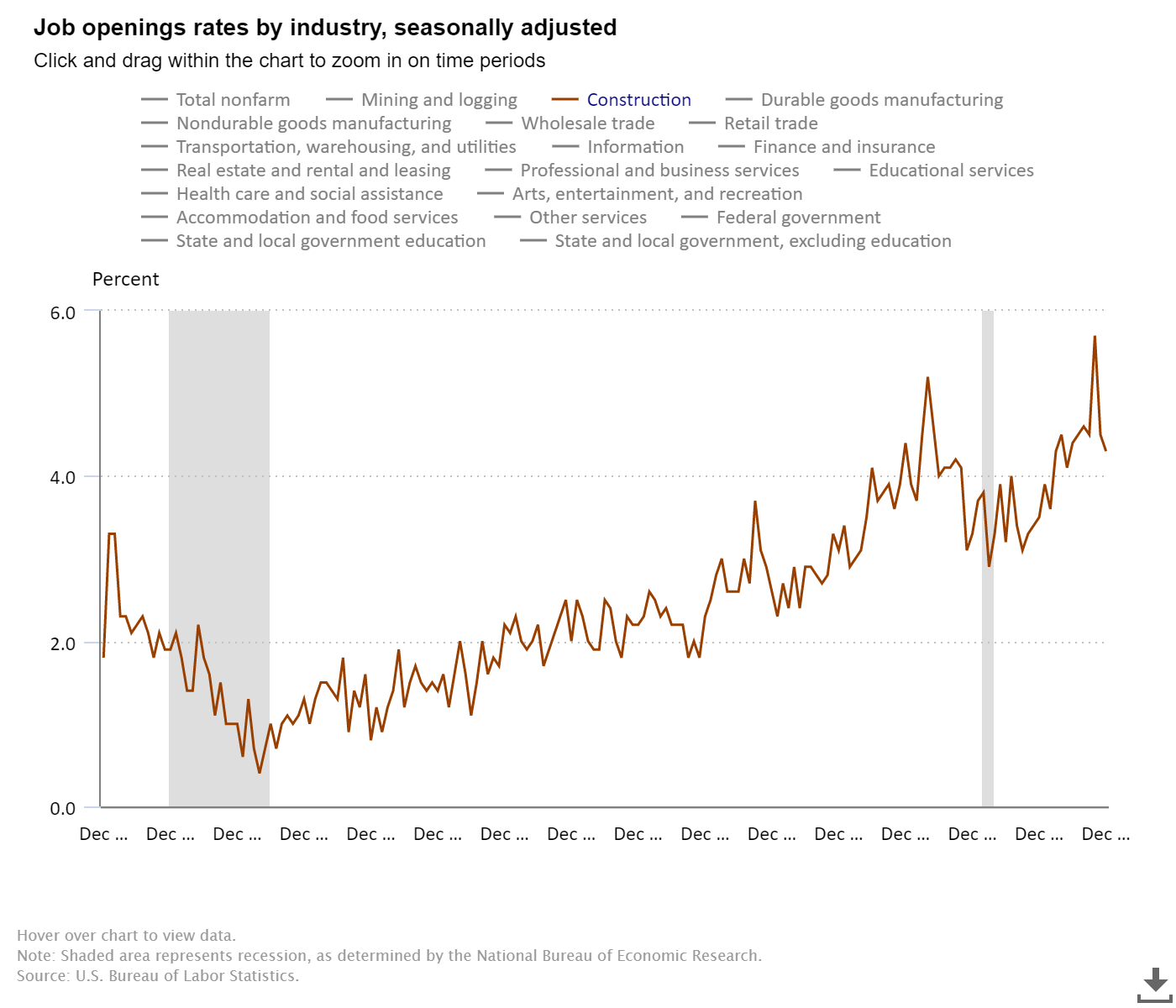

One of the most significant differences between the recovery from the great financial crisis compared to the COVID-19 recovery is that the labor dynamics have been much different this time around. The truth was that we were never going to go into a job-loss recession in 2020 without COIVD-19 and job openings were near 7 million before COVID-19 hit us.

Before the job openings data took off, I was very adamant on Twitter that JOLTS would hit 10 million soon. Job openings are now near 11 million, as the U.S., just like many other countries, has an aging workforce that is difficult to replace. As you see from the chart below, the labor market dynamics from the end of the great financial crisis, where job openings were just a tad over 2 million, weren’t as positive as those we had right before the COVID recession.

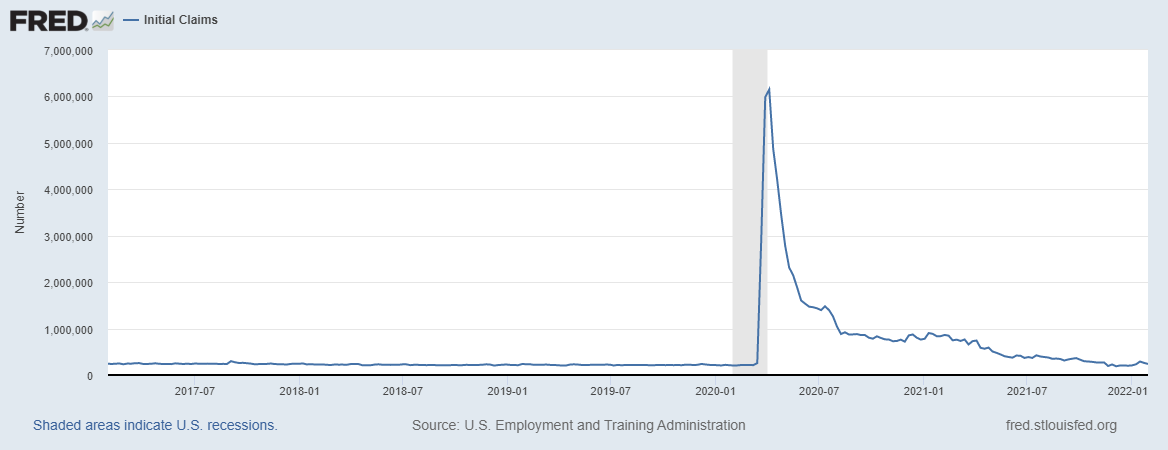

Jobless claims data looks very solid. Even with all the Americans reporting sick due to Omicron, the need for labor in America is massive.

In addition to the America is Back recovery model, I made another call in 2021 on the jobs data. I believed that unlike other economic data, which recovered quickly, the jobs data was going to take some time to get back to pre-COVID-19 levels. So, the target that I set was for September of 2022 or earlier. Now this forecast was before Delta and Omicron. However, not once did I change this forecast due to those due new variants waves.

So, let’s take a look at the numbers today with eight months left until the September report.

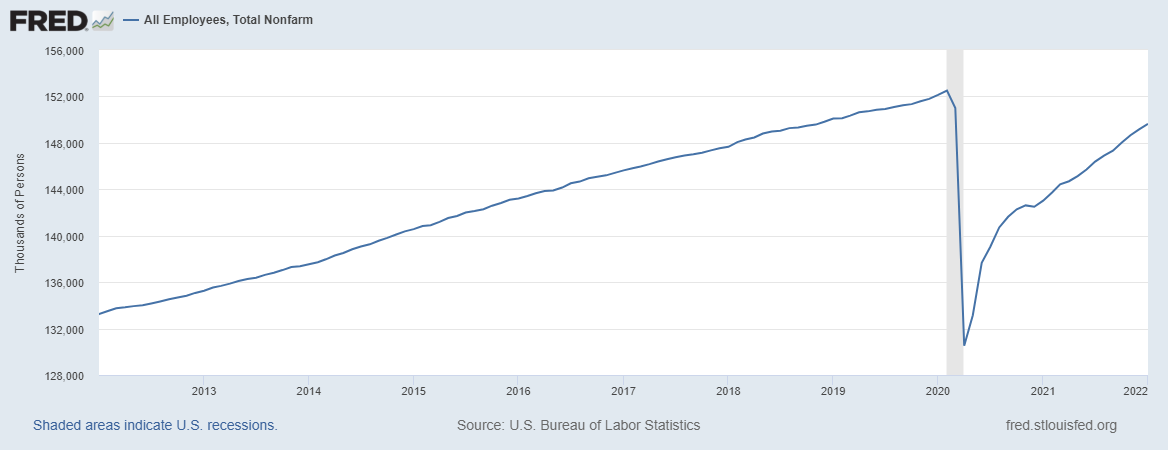

—Feb 2020: 152,553,000 jobs

—Today: 149,629,000 jobs

That leaves us with 2,924,000 jobs left to make up with eight months to go, which means we need to average adding 365,500 jobs per month. The unemployment rate currently stands at 4.0%.

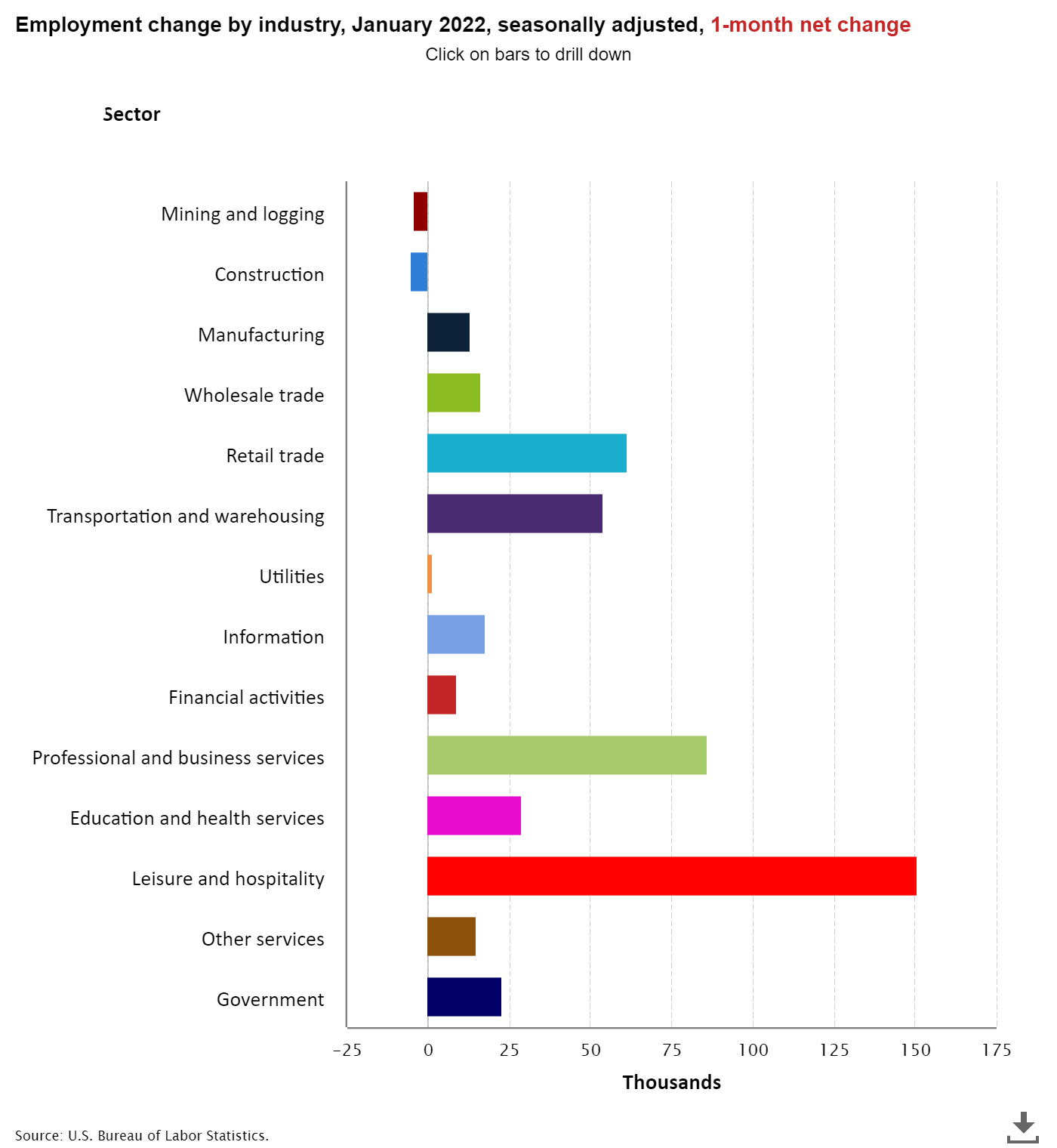

Now this jobs report was such a shocker to the upside that it does have some risk of negative revisions, but still, the trend is your friend and we are still working to get all the jobs back lost to COVID-19. Here is a breakdown of today’s job data. Even though total construction jobs fell, residential construction jobs had another positive month.

Job openings for construction workers are still historically high today as the need for labor in America is very high. So much for the premise that robots and immigrants would take all the jobs in America.

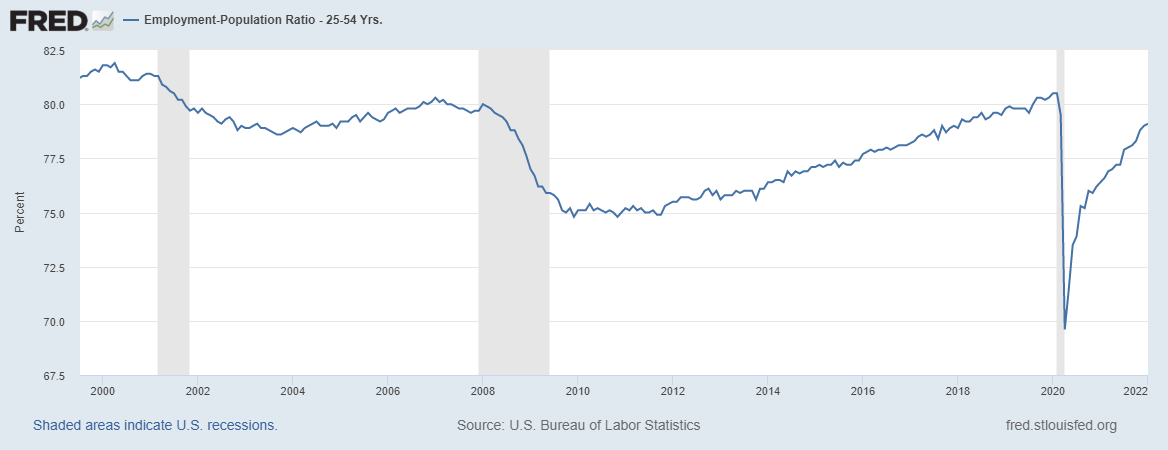

Remember, when looking at jobs data, it’s always about prime-age employment data for ages 25-54. The employment-to-population percentage for the prime-age labor force is 1.4% away from being back to February 2020 levels. The jobs recovery in this new expansion has been much better than we saw during the recovery phase after the great financial crisis.

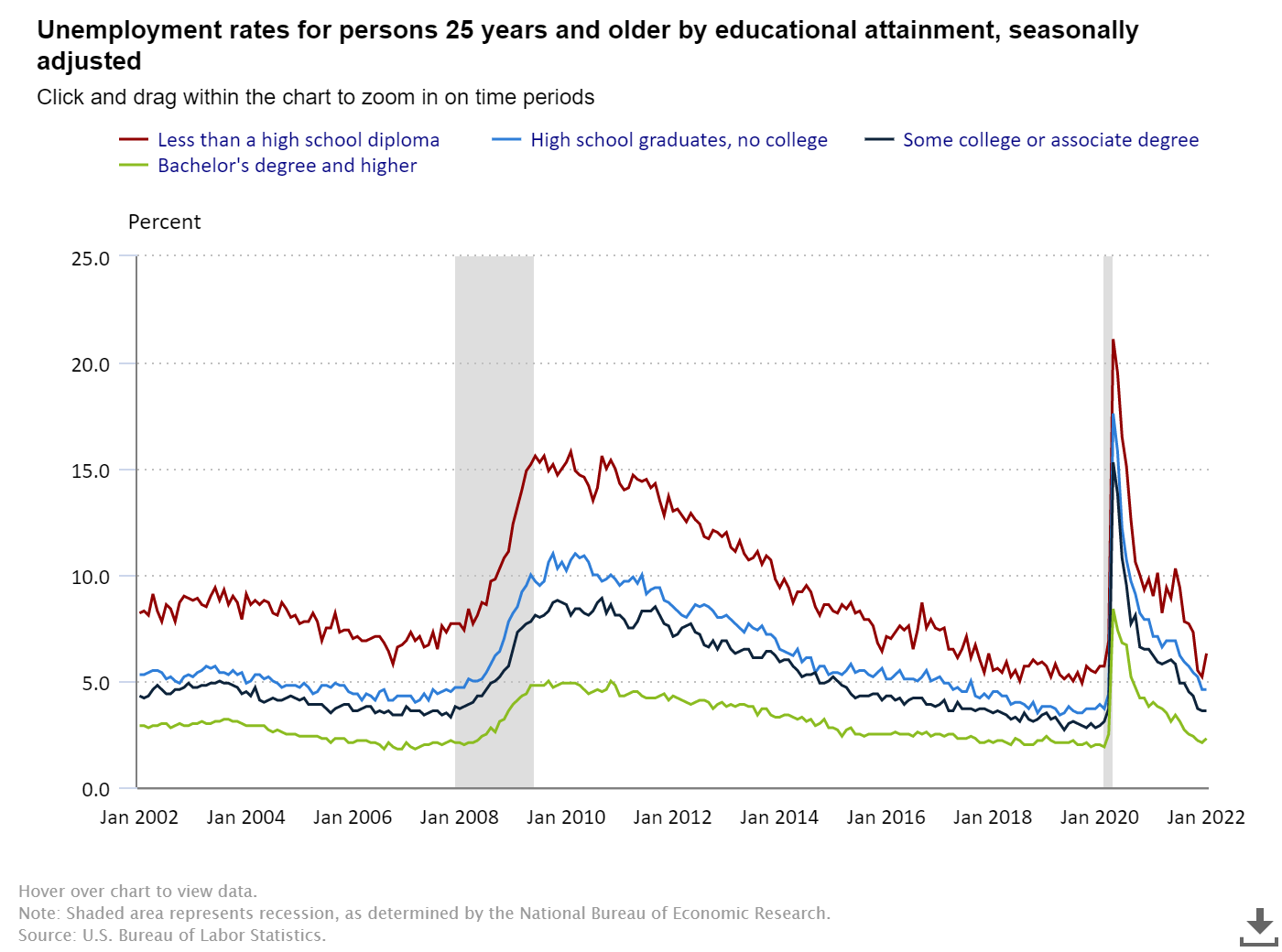

Education and employment

One giant fact that people tend to forget always is that a majority of Americans who want to work have always been working. The part of the labor force with the least educational attainment tends to have a higher unemployment rate. On Twitter, I started the hashtag A Tighter Labor Market Is A Good Thing to remind everyone that the economy runs hot when we have a tighter labor market. We want to see the kind of unemployment rates that college-educated people have spread to everyone because we have tons of jobs that don’t need a college education.

You would always rather have a tight labor market than high unemployment. Hopefully, businesses can invest to create more productivity because the baby boomers are leaving the workforce every month and certain parts of the U.S. don’t have much prime-age labor force growth.

Here is a breakdown of the unemployment rate and educational attainment for those 25 years and older:

—Less than a high school diploma: 6.3%.

—High school graduate and no college: 4.6%.

—Some college or associate degree: 3.6.

—Bachelor’s degree and higher: 2.3%.

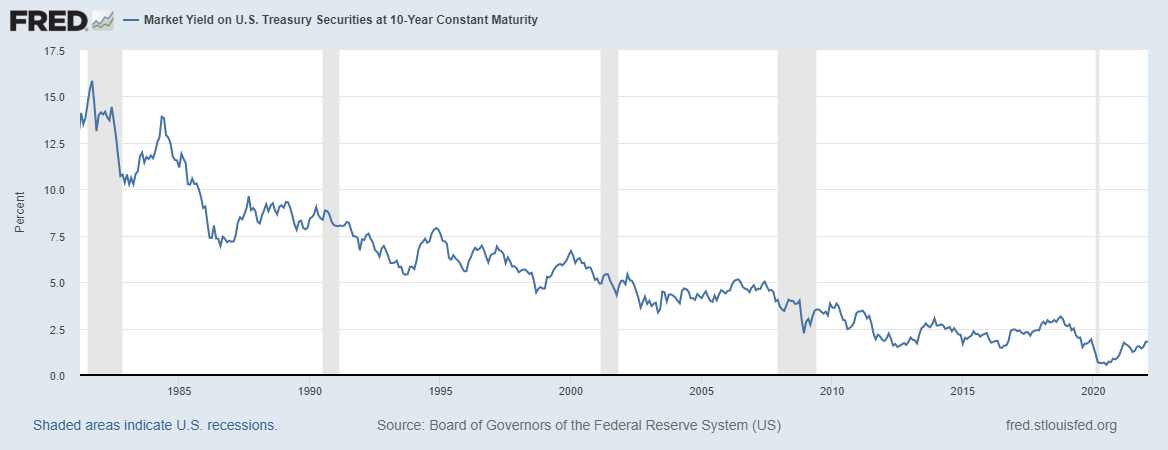

The 10-year yield and mortgage rates

My 2022 forecast said: For 2022, my range for the 10-year yield is 0.62%-1.94%, similar to 2021. Accordingly, my upper end range in mortgage rates is 3.375%-3.625% and the lower end range is 2.375%-2.50%. This is very similar to what I have done in the past, paying my respects to the downtrend in bond yields since 1981.

We had a few times in the previous cycle where the 10-year yield was below 1.60% and above 3%. Regarding 4% plus mortgage rates, I can make a case for higher yields, but this would require the world economies functioning all together in a world with no pandemic. For this scenario, Japan and Germany yields need to rise, which would push our 10-year yield toward 2.42% and get mortgage rates over 4%. Current conditions don’t support this.

The bond market shot up higher as soon as the jobs report came in and currently, at this very second, the 10-year yield is at 1.93%. I totally understand why people are confused why bond yields are still below 2% with the economy running so hot and inflation data being as high as it is. However, as always, I have tried to stress, the trend is your friend. Bond yields and the 10-year yield are just following that long-term trend lower.

With that said, what I want to see is the same thing I stressed in 2019. We need to see the 10 year yield close above 1.94% and follow-through bond yield selling to have conviction that bond yields can go higher. This jobs report was a very big positive for the Untied States of America and global yields, especially in Japan and Germany, are rising. This is the right backdrop for mortgage rates to rise and hopefully create some balance in the housing market because if this doesn’t do it, I see nothing else that can create more days on the market as we are starting spring 2022 with fresh new all-time lows in inventory.

Economic cycle update

Now for an economic update. Some of the economic data has been cooling off as expected. The surge in Omicron cases, while not being able to create the same fear and panic as we had in March and April of 2020, did impact some of the economic data. In general, the rate of growth in some economic data can’t be replicated in 2021, such as GDP and the rate of growth of retail sales. However, the U.S. economy is still in expansion mode with only one of my recession red flags raised.

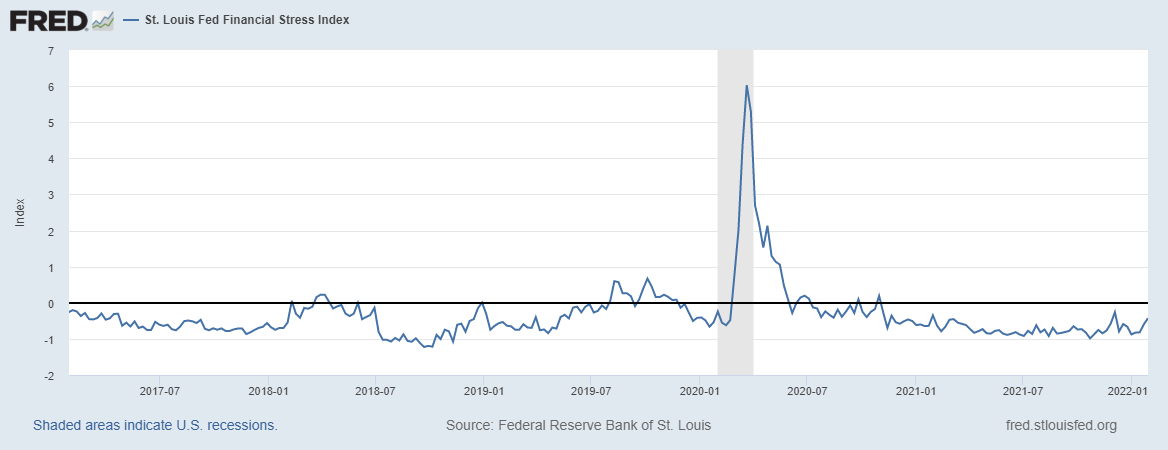

The St. Louis Financial Stress Index, a crucial variable in the AB recovery model, is showing a bit of life lately at -0.4227%. The stock market has been more volatile lately and talks about how many rate hikes are coming in 2022 has perked up the financial markets from their bored state in 2021.

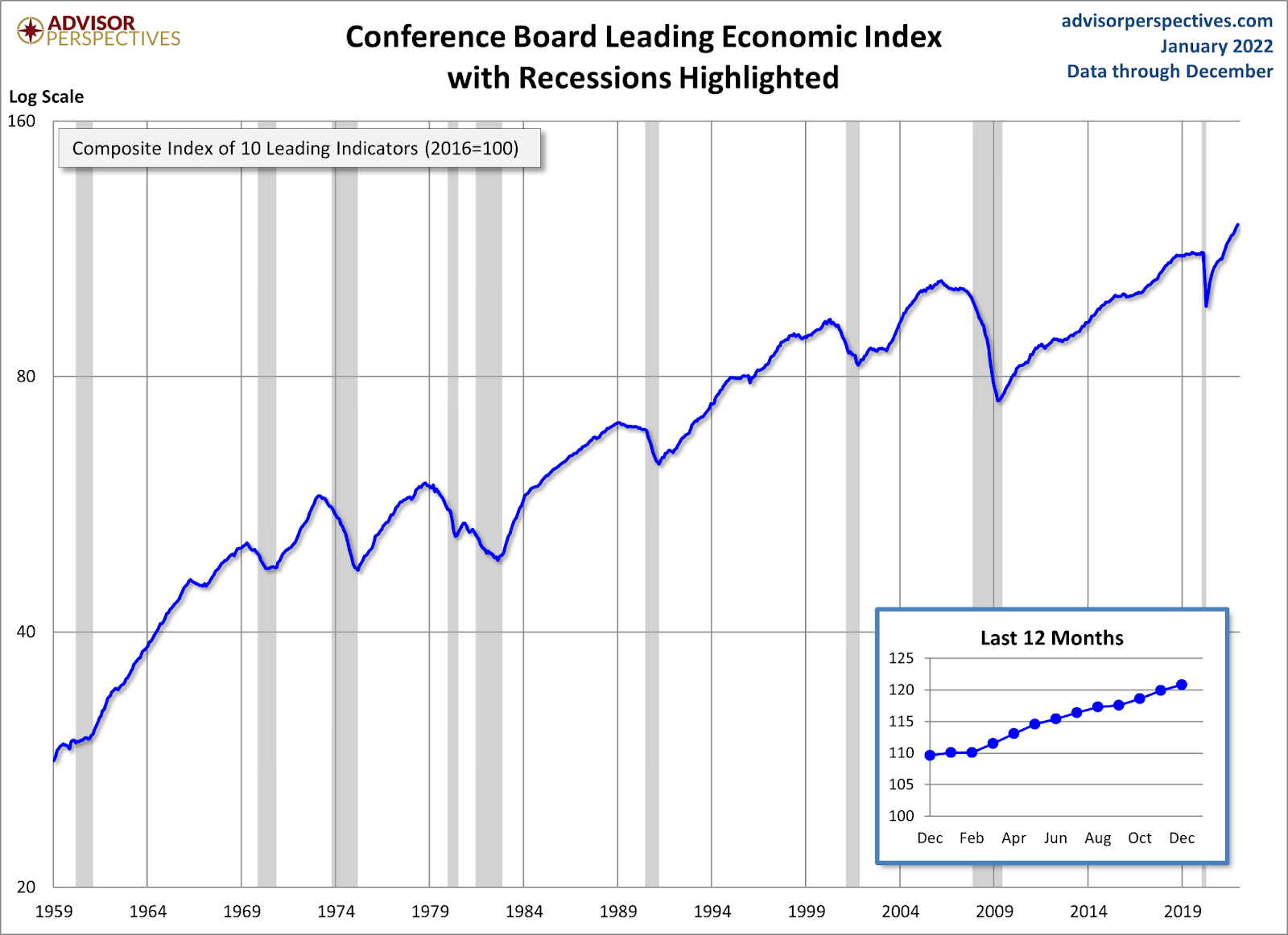

The leading economic index has been very solid lately. When this data line falls for four to six months straight, then the topic becomes different. However, this hasn’t been the case, it bottomed in April of 2020 and has had a sharp rebound.

Retail sales have slowed down, which should have been expected. The rate of growth toward the end of 2020 and 2021 was something spectacular to see — I had anticipated moderation in the data much earlier, but it’s only now showing up.

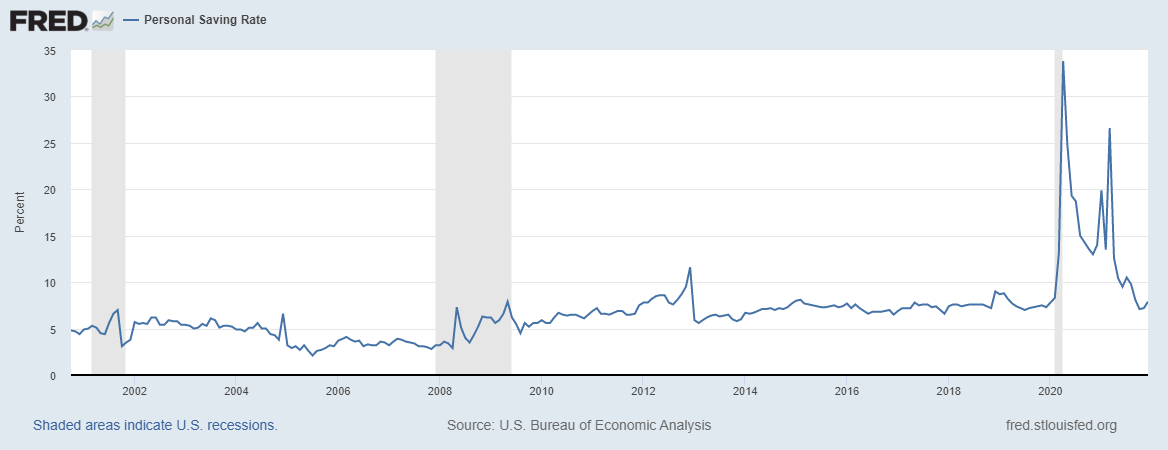

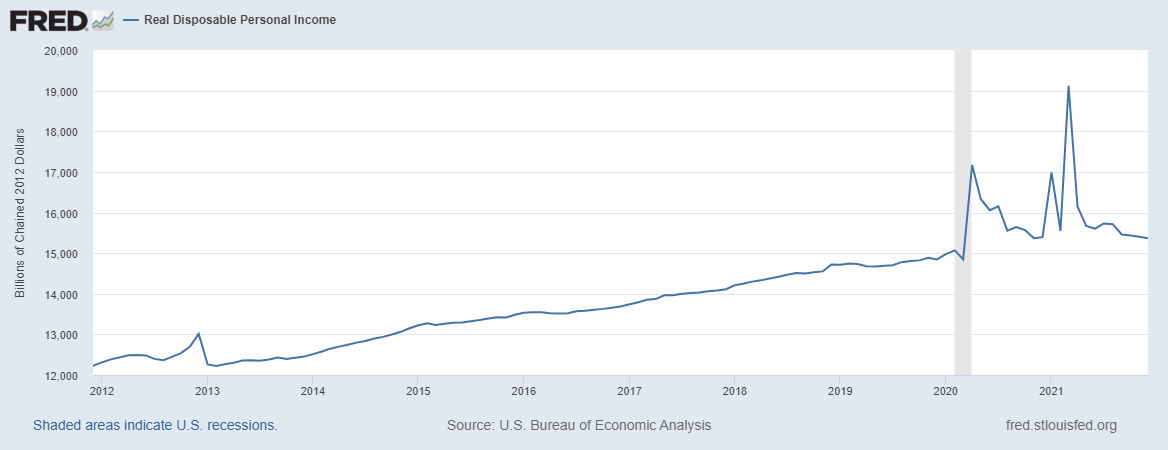

The personal savings rate and disposable income are healthy enough to keep the expansion going! Even though the disaster relief has faded from the economic discussion, both these levels are good to go as employment has picked up a lot from the COVID-19 lows with wage growth.

However, just like I had an America is Back recovery model on April 7, 2020, I have recession models and raise recession red flags as the expansion matures. I raised my first red flag when recently when the unemployment rate got to 4% and the 2-year yield got above 0.56%.

Once the Fed raises rates, the second recession red flag will be raised. My job is to show you the progress of the economic expansion, into the next recession, and out — over and over again. My models don’t sleep! Once more red flags are raised, I will go over each and every single one.

At some point in the future, I will be on recession watch, when enough red flags are up. However, we are not at that time yet. Even though I no longer say we are early in the economic expansion, we are still on solid footing. However, the more exciting thing for me is to see whether we can finally crack over 1.94% on the 10-year yield and try to bring balance to an extremely unhealthy housing market.

The post Positive jobs report sends bond yields higher appeared first on HousingWire.