Just the Facts: Four Key Housing Market Takeaways for This Week

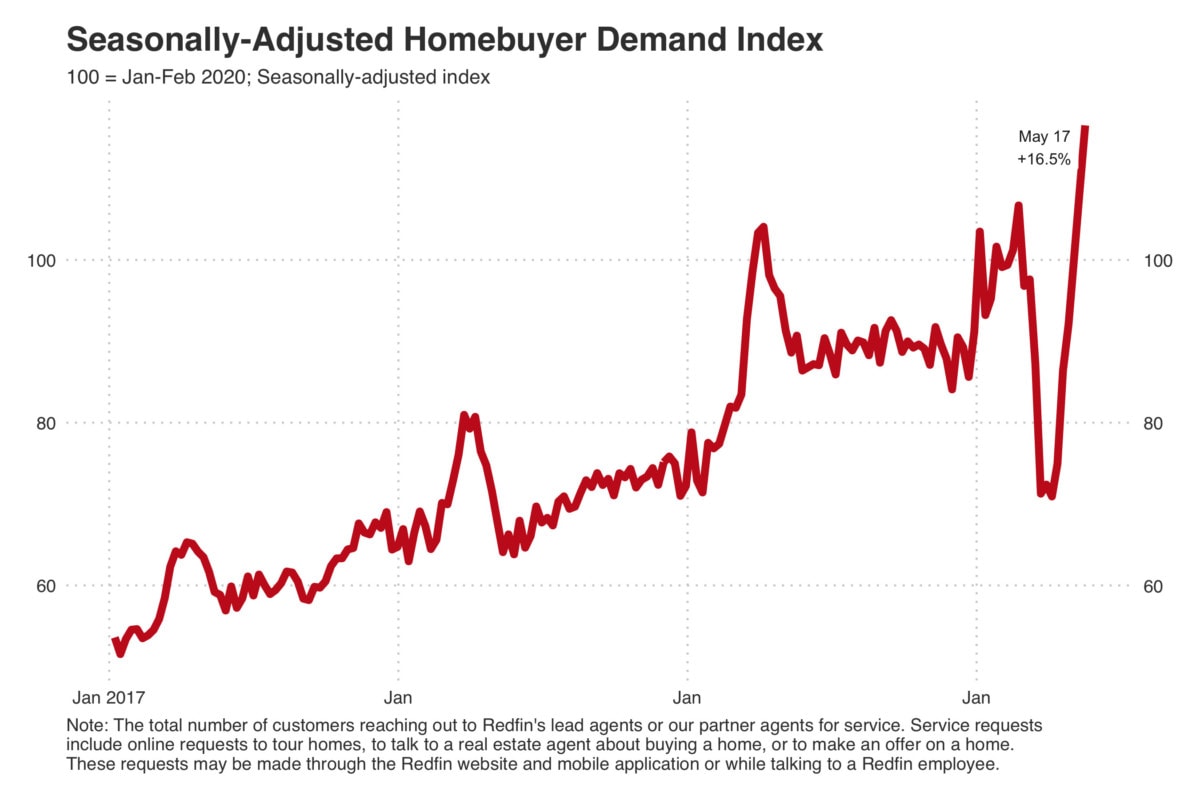

- Home-buying demand is now 16.5% above pre-coronavirus levels on a seasonally-adjusted basis, driven by record-low mortgage rates

- Inventory of homes for sale can’t keep pace with demand. Jerry Diaz, a Redfin agent in Nashville says, “I’m showing a lot of houses, but not selling as many as I could because they’re gone before we can write an offer.” Forty-five percent of the homes under contract in the seven days ended May 15 were on the market less than two weeks

- The migration from expensive metropolitan areas to smaller cities and towns appears to be picking up steam as buyers hunt for more space and lower prices. Tiffany Aquina, a Redfin agent in Virginia said, “People who were considering a move two or three years down the line are pulling the trigger now. I have one client who’s planning to retire early, cash in on high home prices in Virginia and move to South Carolina.”

- Touring homes virtually with online 3D walkthroughs is becoming significantly more popular. For the week of May 10, nine percent of new homes listed for sale had a 3D model created using Matterport technology, up from only 2% in January and February prior to the pandemic

Home-buying demand reaches a new peak as pent-up demand is unleashed

This past week, Redfin’s home-buying demand moved out of recovery mode and into growth mode, reaching a new peak. For the seven days ended May 17, demand was 16.5% higher than it was before the pandemic, on a seasonally-adjusted basis.

To handle the rapid rise in home-buying demand, Redfin has been bringing staff back from the furlough that was initiated in early April. Of the roughly 1,000 people who went on furlough, we’ve already welcomed approximately 350 Redfin employees back to work.

The strength of the recovery has been surprising. New cases of the coronavirus have certainly tapered from their peaks back in April, but over 20,000 new cases are still being reported daily in the U.S. and last week another 2.4 million workers filed for unemployment benefits. Home-buying demand seems to have been largely unaffected in the face of those headwinds.

Mortgage rates have stimulated the housing market, with the average 30-year fixed rate mortgage at record lows of 3%. Now a new report from the Federal Reserve sheds some light on how home-buying demand has strengthened despite unemployment rates that haven’t been seen since the Great Depression. Among respondents in the Fed’s survey, 13% reported a job loss or furlough in March or early April, but that number was 39% for people with a household income less than $40,000.

With the rapid increase in housing prices over the past several years, it’s been increasingly difficult for many Americans to afford the American dream. With job losses disproportionately affecting people with lower incomes, unemployment hasn’t had much effect on home-buying demand, yet.

The migration out of America’s major metropolitan areas is picking up steam

The big question is whether this demand surge will be a quick burst of buyers who deferred their plans during the shutdown or if it’ll last much longer as people hunt for more space and more affordable homes. Search data from Redfin.com suggests that migration from expensive metropolitan hubs to smaller cities and towns has been happening for years, but it seems to be gaining steam since the coronavirus outbreak.

Tiffany Aquino, a Redfin agent in Virginia, said, “The pandemic has people re-evaluating their lifestyle and their goals. People who were considering a move two or three years down the line are pulling the trigger now. I have one client who’s planning to retire early, cash in on high home prices in Virginia and move to South Carolina. Another client is selling her home here to move to Florida full-time to take care of her elderly father. People are putting family priorities first.”

Mike Dusiewicz, a Redfin agent in Connecticut is seeing an influx in buyers who are no longer interested in living in New York City, “The trend over the last 10 years is buyers wanting to be close to the rail lines [into New York], but now the towns further north with good schools are hot.” Buyers are planning to work remotely for the long term, “One of the main questions I get now is ‘how good is the internet up there?’ It won’t be long until listing agents start including Wi-Fi speeds in the marketing materials.” And some buyers can’t get out of the city too soon. “One couple came up to buy a weekend home, but the day the sale was final they moved in and never left. Their lease in the city doesn’t end for eight months.”

More and more, buyers are using digital technology to see homes without having to be there in person. Over the past week, just over 1 in 4 new Redfin clients had their first home showing via video chat and video-chat tours led to 11% of the offers Redfin agents wrote in that same time.

Perhaps the biggest shift in viewing homes is the rising popularity of online 3D walkthroughs that let a buyer tour a home virtually anytime of day or night. For years, Redfin agents have been creating 3D walkthroughs for our clients using Matterport technology. Now the popularity of these 3D scans is surging among other brokers, as well. Nine percent of all new listings that launched the week of May 10 included a Matterport scan and views of Matterport scans on Redfin.com have more than doubled in the last month.

Inventory of homes for sale may be stabilizing after hitting rock bottom in early May

The number of homes for sale is down 23% for the seven days ending May 15, compared to the same period the prior year. But the absolute count of homes for sale inched up each of those days.

Redfin agents across the country are saying the spring market is about to kick off after a two-and-a-half month delay. Some sellers have gotten more comfortable putting their homes on the market and agents have gotten more skilled at showing homes safely while social distancing. Other sellers worry that a second wave of the virus may shut down the economy again later this year and want to list now to take advantage of the strong demand right now.

Low inventory is constraining the number of home sales, but prices are rising

Whether it’s increasing comfort or rising concerns about the future, more sellers put their homes on the market in the seven days ending May 15 than any seven day period since March 25. Over the next few weeks, we’ll see if new listings can keep up with buyer demand and if more inventory leads to an increase in home sales.

For the seven days ending May 15, the number of new pending sales was still down 29% compared to the same period the prior year. That’s an improvement from the 40% declines we saw in mid-April when the market had all but ground to a halt, but still a far cry from normal.

In many markets, there aren’t enough homes for sale, so a lot of the home-buying demand is unmet. Jerry Diaz, a Redfin agent in Nashville says, “I’m showing a lot of houses, but not selling as many as I could because they’re gone before we can write an offer. I feel like I’m standing in the living room with a buyer who decides this is the one and by the time we get out to the car to write the offer, it’s sold.” More than 45% of homes under contract in the seven days ended May 15 were on the market for less than two weeks; five percentage points higher than the same week of 2019.

As a result, prices are rising. The median listing price is up 6% for the seven days ended May 15, compared to the same period last year. Many buyers assumed prices would fall as the pandemic set in, but sellers seem to be holding firm. The increase in home prices and stories from our agents suggest that sellers who don’t sell are more likely to take their home off the market and wait rather than accept a lower price. Some buyers are still out bargain shopping, but are finding there aren’t many deals to be had.

That’s it for this week. If you go out, please stay safe, and if you can, stay home. If you’re out on the front lines, please accept the most sincere thanks from everyone here at Redfin.

The post Home-buying Demand Surges on Record-Low Mortgage Rates; Up 17% From Pre-Coronavirus Levels appeared first on Redfin | Real Estate Tips for Home Buying, Selling & More.