I hear a lot of chatter about a boom in cash-out refinances, and the presumption seems to be that this is destined to wreak havoc on the housing market and the economy at some point. Cash-out loans have been growing over the past few years and it is also true that we have a recent history of excessive equity extraction factoring in a bust in housing. But there are several critical reasons why the recent uptick in cash-out refinancing is nothing like the cash-out boom of the early to mid-2000s.

First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards. Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures.

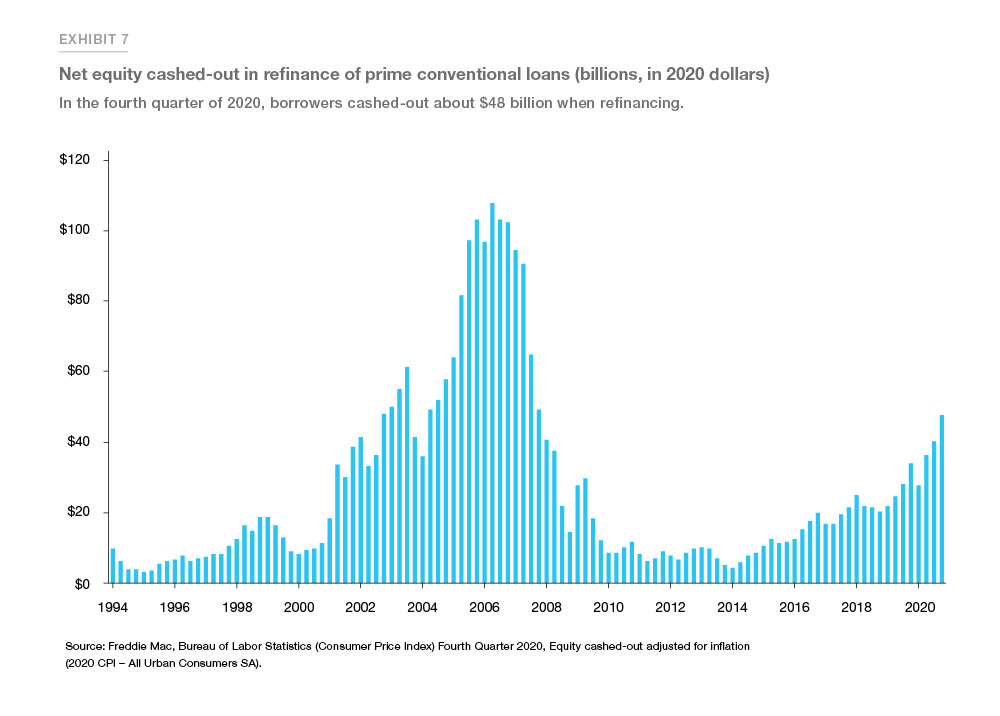

In the 2020 market, on the other hand, refinances were not driven just by an increase in equity but lower mortgage rates. Cash-out loan borrowers who increased their loan balances could get a more favorable rate than in previous years. Although mortgage refinance activity was the highest in 2020 than it has been since 2003, the reasons for refinancing and the quality of the equity loans are much different than they were in the 2000s.

The graph below is from an article by Len Kiefer of Freddie Mac. This is an excellent article for those interested in diving into the minutiae of the 2020 refinance market.

If we dig a little deeper into homeowners’ balance sheets, we see that since 2010, cash flow and loan quality of mortgage holders were excellent.

The post Are we seeing a cash-out refinance crisis? appeared first on HousingWire.