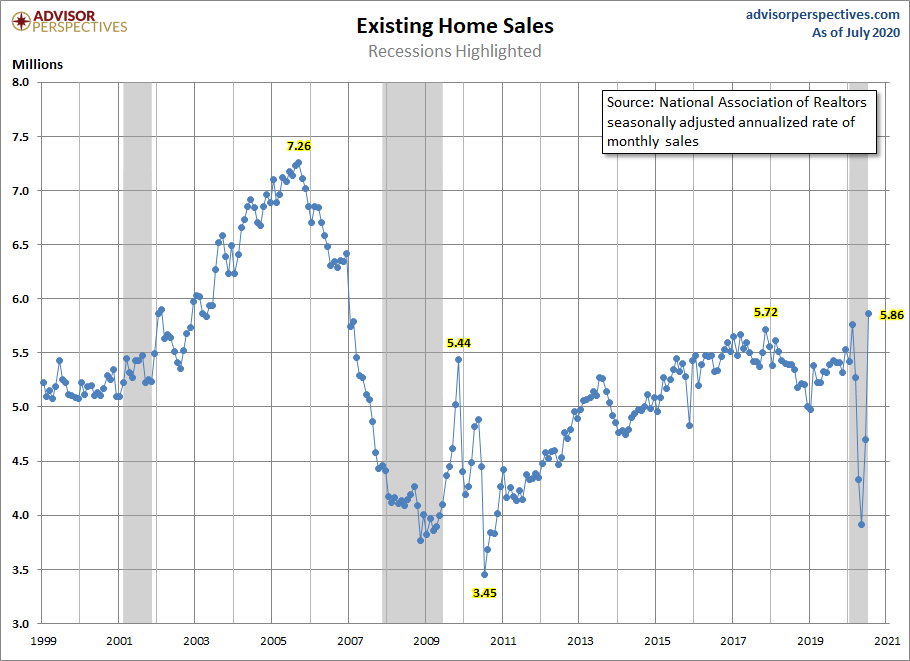

Today, existing home sales blew out estimates, coming in at 5,860,000. With new home sales, pending home sales, housing starts, housing permits, and purchase applications already in v-shape recovery mode, this last metric completes the v-shaped recovery across the board for housing.

Let’s just say this is the final nail in the coffin for the housing bear troll camps that were so sure that this time, housing would finally crash. COVID didn’t get the housing market, but it did pull a fast one on those pesky bears.

Look, I get it. For the casual observers of the market, it may seem intuitive that with all the economic chaos we suffered during the first half of 2020, the housing market would take a drastic hit – from which it would be difficult to recover. Massive job losses and stay-at-home measures seem like a perfect storm for a disastrous housing market.

That belief, however, assumes that one does not understand the two main drivers of housing: demographics and mortgage rates. All that other stuff, my friends, is just stamp collecting. For the last many years I have been writing that the years 2020-2024 would have the best demographics for housing ever recorded in U.S. history. As it happens, these fabulous demographics are accompanied by the lowest mortgage rates ever recorded in history.

This one-two punch is why housing was able to rebound so soundly and will stay stable for some years to come as long as mortgage rates stay below 4.5%.

We saw hints of a flourishing housing market prior to the COVID crisis. In February, for the first time since the start of the century, the U.S. housing market outperformed all other sectors of the economy. I have talked about this before, that the years 2020-2024 would be the time where housing could outperform. Then the massive shock of COVID-19 happened right in the first year of my working thesis.

The fear of the virus and the stay-at-home measures which curtailed the ability to even look at homes put a short-term halt on the promised growth. The floundering economy then caused the mortgage market meltdown in early March, causing mortgage rates to quickly spike. It was crazy for a minute and at that time I needed to keep reminding people that this was a temporary blip that would mostly clear up by July 15. And it did, because none of that chaos changed the fundamentals – demographics were still excellent and mortgage rates were just going lower.

The second part of this story that folks seem to forget is that the existing home sales market only needs 4 million mortgage buyers a year to remain stable. This means only 4 million folks out of the 133 million people working during the worst days of COVID-19 are needed to qualify for a mortgage to keep the market stable.

Compare this to auto sales, which require 16-18 million sales per year to remain stable – and even that sector is rebounding. Note too, that the housing market for the last many years has been composed of 15-20% cash buyers – that is a big chunk of buyers that don’t need a mortgage in order to purchase.

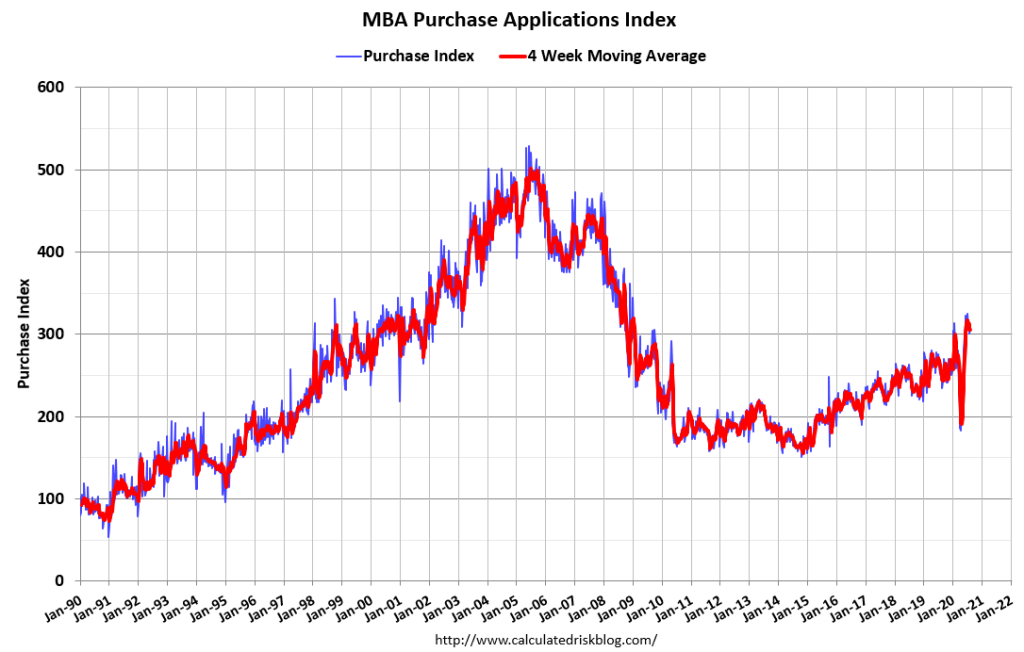

Now, in mid-August, the purchase applications data from the Mortgage Bankers Association continue on the upswing. Year-over-year growth for the last four weeks was +27% +22% +22% +21%, respectively. This is a forward looking demand for 30-90 days.

Having said all of that, housing is still down about 5% compared to last year.

While sales are and will stay elevated compared the COVID-19 lows, the market is not bubbly. This is evident if one compares the purchase application data from the overheating market of 2002-2005 to the period between 2012-2020. Going forward, we don’t need 20% plus growth in purchase applications, on a year-over-year basis, to hold the gains. We just need flat to positive growth in order to maintain our recovery. We have a lot of high-velocity data in our economy so any short-term pullback on housing data, take it in context.

This current existing home sales report does show price growth getting hotter. I’m not extremely worried about this just yet, for two reasons.

First the rate of growth in no way compares to what we had during the bubble years of 2002-2005. And second, we don’t have a consumer credit bubble in the housing market or in the general economy. Real demand growth is limited because lending standards are back to their normal liberal standards which takes away speculation buying on bad debt structures.

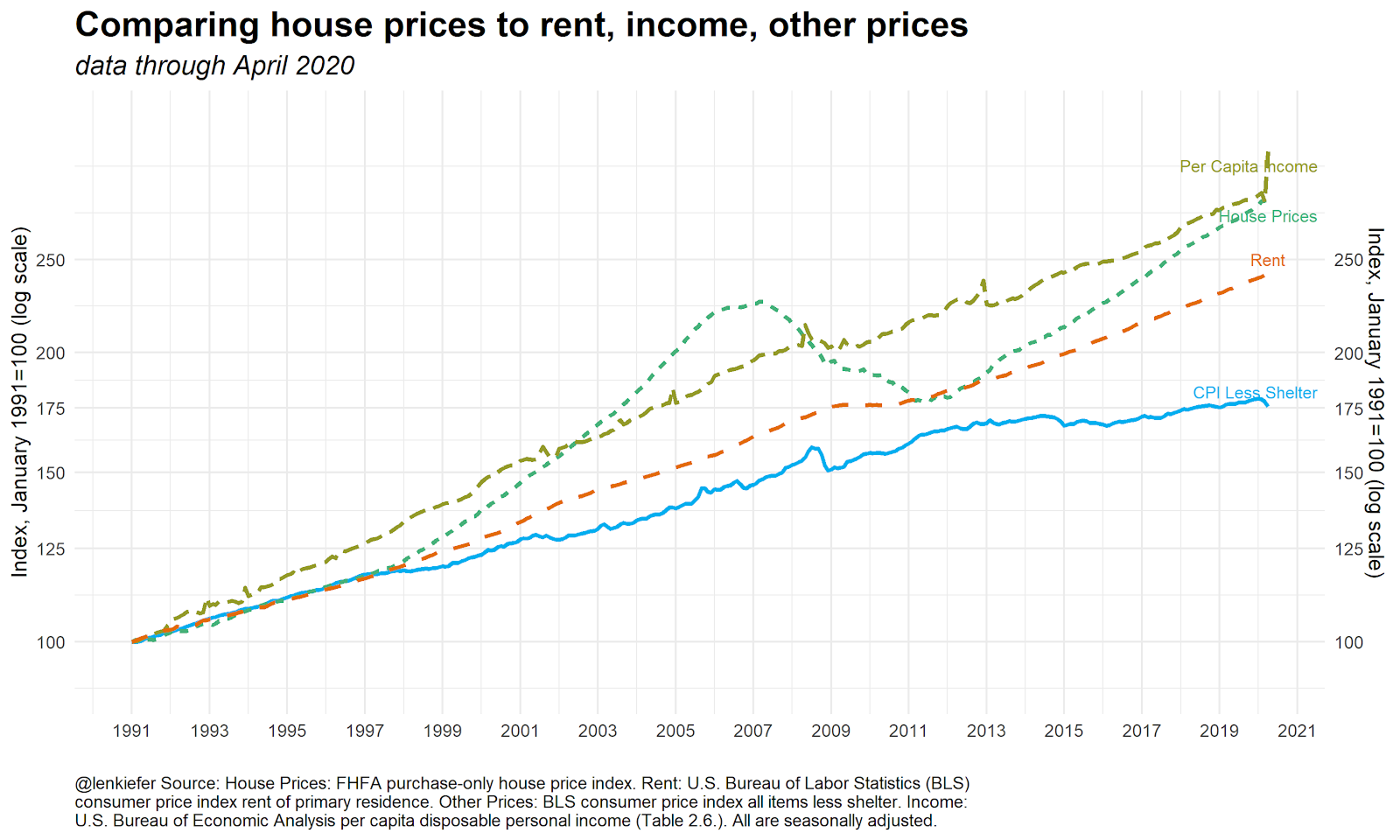

However, home price growth is a developing story that we will need to keep an eye on because we are pushing the limits of per capita income and home prices. This is why I am always rooting for negative real home price growth this decade.

One last thought — the AB (American is Back) model that I introduced in a Housing Wire article back in April 7 is looking a lot better now than it was back then.

If you are one that believes in economic models instead of conspiracy theories, keep following!

The post Are existing home sales showing a housing bubble? appeared first on HousingWire.